How COVID-19 Will Shift Business and Consumer Behavior and Attitudes

The COVID-19 pandemic and its economic fallout drastically changed Americans’ attitudes and behavior at home and at work. Business and consumer practices have shifted substantially under COVID-19 as people and businesses adapt to a socially-distanced world. Origin Ventures attempted to gauge the impact of the pandemic and economic fallout on businesses and consumers and see which changes were likely to persist, and which would fall back to “business as usual.” To do so, we asked our community a series of questions about the impact of the pandemic on their attitudes and habits1. A summary of findings and select results and analyses are presented here.

Summary

Business:

B2C companies may have a brighter outlook than B2B

Both B2B & B2C relatively optimistic: only 33% and 15% (respectively) expect their budgets to decline

Many believe amount of revenue lost due to COVID is decreasing

Physical/in-person service providers may be an exception

Large increase in employees working remote

Increase in willingness to spend on software

Consumer:

Food delivery impacted in both directions

Increase in at-home cooking, DIY hair care, and outdoor time

Increase in remote work and online shopping

Decrease in gatherings, event attendance, in-restaurant dining, and travel for pleasure

COVID-19 Business Impact

Many businesses have allowed and encouraged their employees to work remotely since the beginning of the pandemic. Going forward, 87% of business respondents predicted they’d allow employees to work remotely “more” (28%) or “significantly more” (59%) after shelter-in-place restrictions are lifted. When asked in a free-response question what adaptations they have made to their business as a result of COVID, respondents mentioned an increase in remote work 7 times more than the next-most mentioned adaptation.

As employees work from home in increasing numbers, it becomes critical that they are able to do so efficiently and effectively. Many companies look to software to help employees do their jobs well, no matter where they are: 40% of business respondents predicted they’d pay “more” (32%) or “significantly more” (8%) for software platforms after shelter-in-place restrictions are lifted, while only 8% said they’d pay “less” (none said “significantly less”).

Is Lost Revenue Decreasing?

While businesses have lost significant revenue to COVID-related customer churn and lost pipeline, most believe the worst is behind them: 36% of business respondents say COVID-related churn and lost pipeline is “decreasing” (23%) or “significantly decreasing” (13%) compared to the first 2 months of the pandemic, while only 14% say it is “increasing” (13%) or “significantly increasing” (1%). However, companies that provide a physical/in-person service or experience may be an exception: 29% of those respondents believe COVID-related churn is increasing or significantly increasing (vs. 5% of respondents of other business types) and 28% believe it is decreasing (vs. 38% of respondents of other business types).

B2B Not Predicting Doom; B2C Optimistic

In our survey responses, B2C businesses seem to predict smoother sailing in the near future than their B2B counterparts. 41% of B2C respondents predict they will hire new employees “more” (32%) or “significantly more” (9%) than they did before COVID, compared to 20% of B2B respondents (20% and 0%, respectively). Only 14% of B2C respondents predict they will hire new employees “less” (14%) or “significantly less” (0%), compared to 24% of B2B respondents (20% & 4% respectively). These results are displayed below.

B2C respondents were also more optimistic about their upcoming budgets. 41% of B2C respondents predicted that the next time their budget was set, it would “increase” (37%) or “significantly increase” (4%), compared to only 21% of B2B respondents (17% and 4%, respectively). Only 15% of B2C respondents predicted their budget would “decrease” (15%) or “significantly decrease” (0%), compared to 33% of B2B respondents (26% and 7%, respectively). These results are displayed below.

The optimism that B2C decision-makers feel about their future business may be validated by the results of our consumer spending study, as consumers predicted making more online purchases and other spending increases.

COVID-19 Consumer Impact

Consumers’ behaviors and attitudes have also changed as a result of COVID-19. Some behavioral shifts that one would expect in a socially-distanced world are supported in our data: 74% of consumers predict they will work remotely “more” (30%) or “significantly more” (44%) than pre-COVID, and 73% of consumers predicted they would attend large in-person events like concerts and sporting events “less” (29%) or “significantly less” (45%).

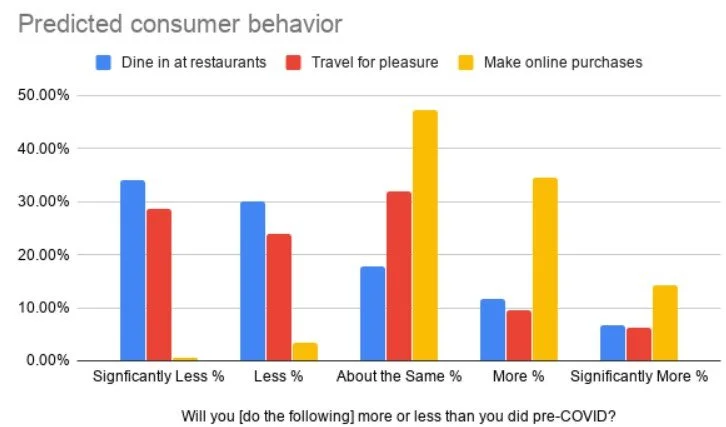

Though respondents predicted other habits would be a bit harder to break, most predicted less public interaction than pre-COVID. 64% said they would dine in at restaurants “less” (30%) or “significantly less” (34%) (19% responded “more” (12%) or “significantly more” (7%)); 53% predicted they would travel for pleasure “less” (24%) or “significantly less” (29%) (16% responded “more” (10%) or “significantly more” (6%)); and 48% predicted they’d make online purchases “more” (34%) or “significantly more” (14%) (4% responded “less” (3%) or “significantly less” (1%)). The graph below shows the results of these questions

Food Delivery during COVID-19 is Polarizing

Food delivery services was a polarizing survey topic, though an uptick in spending was predicted slightly more often than a downtick (“Significantly more”: 8%; “More”: 31%; “About the Same”: 37%; “Less”: 19%; “Significantly Less”: 6%). Full results are graphed below.

The most insightful consumer responses came in the free-response sections, which asked “What services are you likely to do yourself that you weren’t before COVID?” and “How do you expect your leisure time to change compared to pre-COVID?”

COVID-19’s Impact on Leisure: DIY Hair Care, More Time Outdoors

While the 16 answers to what services respondents are more likely to DIY than pre-COVID ran the gamut from the expected (18 respondents replied they would “Cook more at home”) to the niche (2 respondents replied they would do all dog grooming themselves) – the most common response was a bit unexpected: hair care.

19 respondents replied that they would cut or style their own hair, whereas pre-COVID they visited a salon. An additional 7 responses mentioned non-hair related grooming (most commonly manicures and pedicures). As venture capitalists, we wonder if this behavior change could be a boon for direct-to-consumer grooming companies like Birchbox or Madison Reed.

The 31 different responses to how respondents’ leisure time would change compared to pre-COVID included both negative responses (“fewer or smaller gatherings” was submitted 23 times, “less travel” 18 times, and “less eating/drinking out” 10 times) and positive ones (“more time at home” 9 times, and “more time with family/close friends” 7 times). The most insightful output may be that “more time outdoors” was the most-submitted positive change of the survey, with 12 submissions. Geography and seasonality likely affect this response, but we wonder if there is a positive correlation between COVID-related lockdowns and increased consumer spending on outdoor goods.

We appreciate everyone who took the time to respond to the survey. We will leave the survey open to new submissions indefinitely, and will solicit new submissions periodically to better compare behavioral and attitudinal changes over time as COVID-related restrictions continue.

If you’d like to access the full dataset that drove this analysis, email devon@originventures.com with “survey data” in the subject line.

Origin Ventures distributed this survey via its email marketing list as well as on Twitter and LinkedIn. Respondents were self-selected. Survey responses were gathered between July 13th and 29th. Business n=82, Consumer n=149